By Ronald Wortel, MBA, P. Eng.

READ THE FULL TRX RESEARCH REPORT

TRX Gold Corporation (NYSE:TRX) (TSX:TRX.TO) is a junior gold producer operating the Buckreef Gold Mine in Tanzania under a joint venture with the state mining development company.

An investment in the Company gives leverage to a growing production profile based on a sound PEA business plan, capitalizing on higher gold prices and the ability to be self-funded. This plan sees production growth from 27,000 to over 90,000 ounces per year over the next five years. This strong growth profile is expected to attract additional market interest in the Company.

Our valuation is primarily based on a discounted cash flow NAV analysis for the Company based on its 55% ownership in the Buckreef Gold Mine and the projected PEA growth plans and industry metrics. Our 12-month fair market value target price is US$1.00.

The Company’s proven operational execution with scalable production growth is highlighted by three production expansions (120 to 2,000 tpd) that were completed on time, on budget, and funded from internal cash flow.

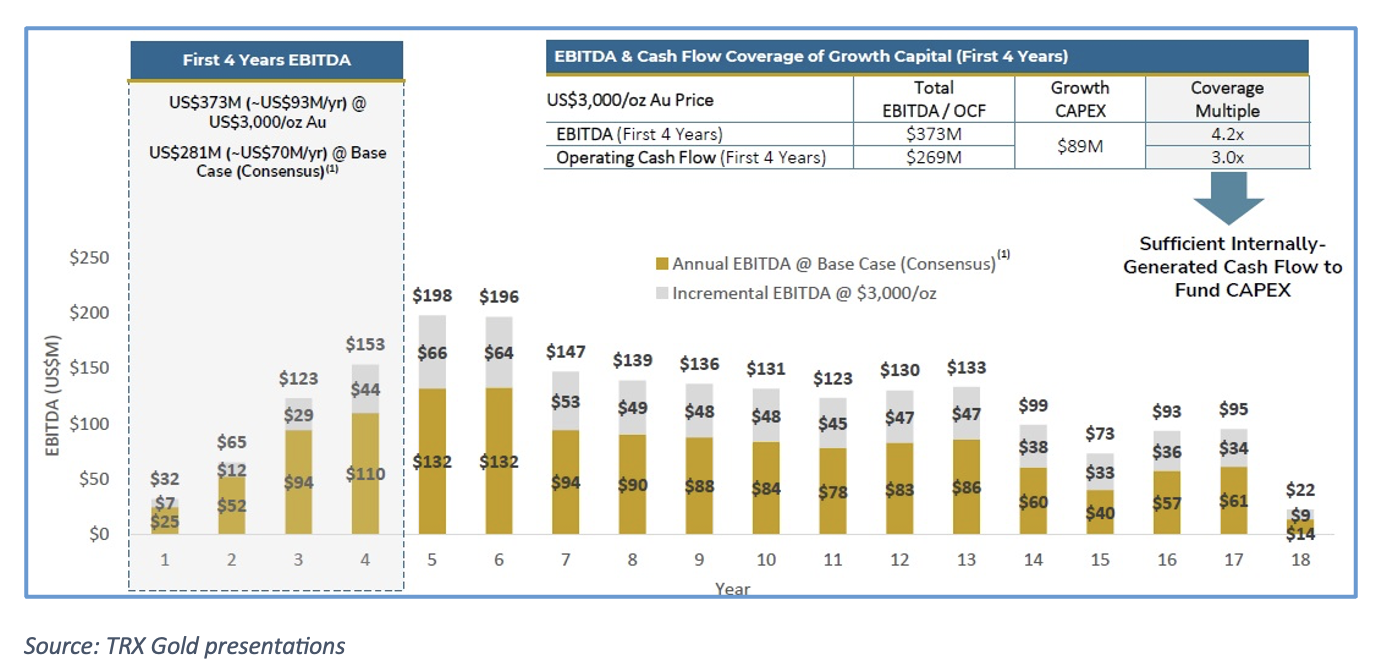

The next phase of growth was outlined in a Robust PEA that establishes a long-life, high-margin mine plan. In April 2025 a PEA outlined a 62,000 oz/year operation lasting 17.6 years with an estimated NPV5% of US$1.2B pre-tax / US$766M post-tax at US$3,000/oz. The modelled all-in sustaining costs (AISC) of US$1,206/oz justifies a high-margin profile even at conservative gold prices. The US$89M growth capex is fully funded by internal cash flow—no equity dilution anticipated for expansion.

Despite these strengths, TRX Gold remains undervalued relative to its peers, trading at ~0.29x P/NAV and ~0.98x EV/2027E EBITDA versus peer group averages of ~0.57x and ~3.3x, respectively. As the Company continues to execute on its production growth plan, deliver on PEA milestones, and demonstrate exploration success, we believe this valuation gap presents a clear re-rating opportunity. In our view, TRX Gold combines near-term cash flow strength, long-life production visibility, and disciplined capital stewardship—positioning it as a compelling growth story in the junior gold producer sector.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.