Lantheus Holdings, Inc. (NASDAQ: LNTH) reported first quarter 2026 financial results on May 7th. Revenue was $377 million, up 1% from 1Q:25 but down 7% sequentially. Adjusted fully diluted earnings per share were $1.46, falling 5%. Full year 2026 guidance remains the same as issued in late February: revenues between $1.4 and $1.45 billion and adjusted earnings per share of $5.00 to $5.25. First quarter growth in Definity and Strategic Partnerships was partially offset by declines in Pylarify revenue. However, the addition of revenue from NeuraCeq compensated for the loss of SPECT revenues, which were divested on January 1st. At quarter-end, cash and equivalents were $499 million compared to $359 million at the end of 2025. Operating cash flow and proceeds from the sale of the SPECT business were only partially offset by cash used in financing, generating a net contribution of $139 million during the first quarter.

At the beginning of the year, prior Chairperson of the Board and former CEO, Mary Anne Heino, returned as the interim chief executive following the retirement of Brian Markison. Her return ushers in a new strategic focus to prioritize investment in the development and commercialization of innovative PET radiodiagnostics, alongside a decision to pursue value‑maximizing alternatives for radiotherapeutic assets to support long‑term growth. The company notched several successes since the beginning of the year, with approval of Pylarify TruVu and tentative approval for PNT2003 in March. The target action date for Octevy was extended by three months to June 29th, 2026, in order for the FDA to review manufacturing-related information.

See below for links to key materials related to first quarter 2026 results:

1Q:26 Financial and Operational Results

Lantheus’ earnings release on May 7th, 2026, was followed by a conference call which included interim CEO Mary Anne Heino, CFO Bob Marshall, and Chief Commercial Officer Amanda Morgan. The team highlighted its strategy of maintaining market leadership in PSMA PET, building momentum for NeuraCeq, advancing Lantheus’ late-stage clinical portfolio, and maintaining disciplined capital allocation. A financial comparison for 2025 follows.

For the quarter ending March 31st, 2026, relative to the prior year:

- Net sales were $377 million, up 1.2% from $373 million. The increase was driven by the addition of $35.4 million in NeuraCeq revenue and a 6.8% increase in Definity sales. Pylarify revenues declined 6.5% to $241 million as price declines of ~12% were only partially offset by 5.8% volume growth. The sale of the SPECT business on January 1st was also a detractor, as TechneLite, NeuroLite, Xenon Xe-133 gas, and CardioLite were all divested to SHINE. The remaining line item, Strategic Partnerships and Other, rose 52% in the quarter to $16.3 million due to the addition of CDMO services from the Evergreen acquisition;

- Cost of goods sold rose 8% to $146 million, and gross margin declined to 59.4% from 62.7% due to lower prices for Pylarify.[1] Pylarify’s margin impact was offset by the removal of lower margin SPECT revenues and their replacement with higher margin NeuraCeq revenues. Other offsets to the margin decline include the contribution from MK-6240 sales for investigational use and an increase in Definity sales volume;

- Sales and marketing expenses were $52.7 million, up 24% from $42.5 million, driven by higher costs related to NeuraCeq sales, and marketing expenditures related to launch preparations, primarily for Pylarify TruVu;

- General and administrative expenses were $57.5 million vs. $56.8 million, increasing 1%. The change was attributable to the acquisitions of Life Molecular and Evergreen. Higher professional fees and employee-related costs, such as stock-based compensation, also contributed. These increases were offset by lower litigation costs and a legal settlement received in 1Q:26;

- Research and development expenses were $39.4 million, up 8% from $36.3 million. The increase was related to additional costs related to the Life Molecular and Evergreen acquisitions. An increase in project costs related to LNTH-2403 also contributed. Increases were offset by the absence of a $5.4 million payment that was made to Lantheus Biosciences for LNTH-2401 that occurred in the prior year;

- Interest expense was $4.9 million, up from $4.8 million in the prior year, and relates to the 2.625% convertible notes;

- Other items generated a gain of $80.0 million vs. a loss of $734,000 due to the gain on the sale of the SPECT business, an increase in equity value for investments in Perspective and Radiopharm Theranostics, and other miscellaneous income;

- Income tax expense of $38.0 million represents a 24.3% tax rate, with state income taxes, nondeductible stock compensation, and non-deductible acquisition-related costs contributing to the difference between the reported rate and the U.S. statutory rate of 21%. This was partially offset by tax credits;

- GAAP net income was $118 million or $1.80 per diluted share. Adjusted net income as presented by Lantheus was $95.8 million or $1.46 per diluted share. The majority of the difference is explained in part by the removal of stock and incentive plan compensation, gain on sale of the SPECT business, investment gain from equity holdings, acquisition, integration, and divestiture-related items, and the income tax effect of these non-GAAP adjustments.

On March 31st, 2026, Lantheus held $499 million in cash and equivalents compared to $359 million at the end of 2025. Free cash flow for 1Q:26 was $122 million vs. $99 million in 1Q:25. Lantheus recognized an additional $29 million in investing cash flows from the sale of SPECT and the sale of other assets.

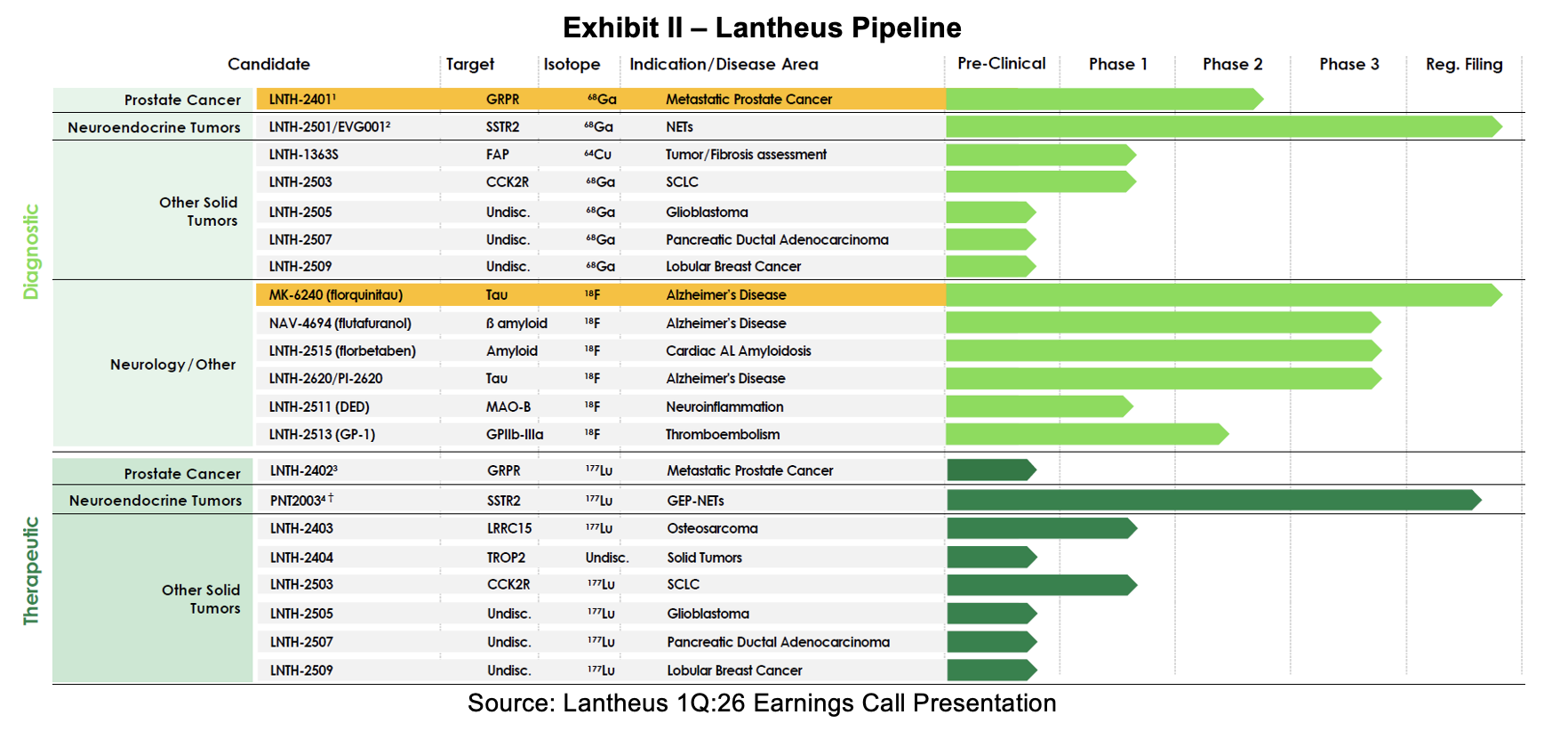

Pylarify TruVu

Lantheus announced that it was developing a new formulation of Pylarify last year and disclosed that it had been submitted to the FDA for review in August 2025. It was submitted using the 505(b)(2) regulatory pathway and later approved on March 6th, 2026. The new formulation, called TruVu, contains a new radiolytic stabilizer that enhances product stability at higher radioactive concentrations. The change is expected to increase batch size by 50% and supports higher radioactive concentrations, which improve efficiency and distribution. Manufacturing TruVu requires PET Manufacturing Facilities (PMFs) with high-energy cyclotrons. According to Lantheus, approximately 70% of their PMF network has these cyclotrons in place. As the company prepares to roll out TruVu, it will execute a technology transfer across its partner PMFs. Following a conversion of a PMF to TruVu, legacy Pylarify will no longer be manufactured. In addition to ensuring that the PMFs are ready for manufacturing, Lantheus will also ensure that customers are prepared for the change and that coding and insurance coverage are in place prior to sale. TruVu should be a strong contributor to 2027 growth, and it will benefit from a reset of transitional pass-through (TPT) status. TPT is a reimbursement medium used for outpatient payments that provides a three-year period of additional reimbursement for certain new medical technologies.

NeuraCeq

NeuraCeq was a strong positive contributor in the first quarter of 2026. It was part of the acquisition of Life Molecular Imaging and first contributed revenues to Lantheus’ income statement in 3Q:25. Sequential growth has been strong, with 14% growth in the first quarter. Revenue growth for the beta amyloid imaging agent was driven by increased utilization within existing accounts and from the ongoing adoption of Alzheimer’s disease-modifying therapies. Since Lantheus acquired LMI, it has expanded the manufacturing footprint and leveraged Lantheus’ existing relationships.

Other Key Assets

Octevy was acquired as part of the Evergreen merger and is also known as LNTH-2501. It is a registrational stage PET diagnostic imaging agent targeting neuroendocrine tumors. Evergreen had submitted the application to the FDA for review and a Prescription Drug User Fee Act (PDUFA) date was assigned for March. The FDA extended this date to June 29th, 2026 to allow it additional time to review manufacturing-related information. Management indicated that the delay was unrelated to product safety or efficacy and expects Octevy to be commercially launched in early 2027.

PNT2003 received tentative FDA approval on March 2nd, 2026. It is a Lu-177 dotatate radioequivalent of Lutathera. It is indicated for the treatment of somatostatin receptor-positive gastroenteropancreatic neuroendocrine tumors (GEP-NETs), including foregut, midgut, and hindgut neuroendocrine tumors. Lantheus anticipates launching the product with consideration of the Hatch-Waxman 30-month stay,[2] disposition of legal proceedings, and execution of a successful manufacturing and commercial strategy.

Corporate Milestones

- Completion of SPECT business unit transfer to SHINE – January 1st, 2026

- Reformulated Pylarify approval – March 6th, 2026

- Target Action Date for LNTH-2501 (Octevy) in SSTR+ NETs – June 29th, 2026

- Launch six additional PET Manufacturing Facility (PMF) sites in support of NeuraCeq – 2026

- Target action date for MK-6240 – August 13th, 2026

- MK-6240 market launch – 2H:26

- FDA approval and launch of PNT2003 after Hatch-Waxman resolution – 2026

- Launch of reformulated Pylarify (TruVu) – 4Q:26

- Commercial launch of LNTH-2501 (Octevy) – 2027

Summary

Lantheus delivered a modest 1.2% year‑over‑year revenue increase in the first quarter, driven primarily by the addition of NeuraCeq, continued Definity growth, and a sharp rise in Strategic Partnership and Other revenues. These gains were partially offset by Pylarify price declines and the impact of the SPECT business divestiture, which together muted top‑line momentum.

Despite the slight revenue lift, adjusted earnings declined, reflecting lower Pylarify pricing and reduced operating leverage, though this was partially cushioned by a lower share count and strong cash generation. Free cash flow benefited from the SPECT divestiture, which bolstered the company’s cash position.

Regulatory progress was a major highlight of the quarter. The FDA approved Pylarify TruVu, a next‑generation PSMA PET formulation designed to enable larger batch sizes at high‑energy cyclotron sites, with a phased launch expected to begin in late 2026. The company also received tentative approval for PNT2003, a radioequivalent therapy for gastroenteropancreatic neuroendocrine tumors. Meanwhile, the review of Octevy was extended as the FDA requested additional time to evaluate manufacturing‑related information.

Management reiterated that these regulatory milestones are expected to set the stage for accelerated growth in 2027, following what is likely to be a transition and rebuilding year in 2026 as TruVu conversion ramps and pipeline launches begin to contribute.

Looking ahead, Lantheus is increasingly concentrating its strategy around PET radiodiagnostics, having divested its SPECT business and signaling that it may monetize certain radiotherapeutic assets to sharpen its focus. The company is also investing heavily in neurology imaging, including Alzheimer’s-related diagnostics, which management views as a significant long‑term growth engine given rising demand for disease‑modifying therapies and earlier detection.

Lantheus advances through 2026 with a strengthened balance sheet, a deep and advancing pipeline, and multiple regulatory catalysts that support a multi‑year growth trajectory anchored in next‑generation imaging technologies.

SUBSCRIBE TO ZACKS SMALL CAP RESEARCH to receive our articles and reports emailed directly to you each morning. Please visit our website for additional information on Zacks SCR.

DISCLOSURE: Zacks SCR has received compensation from the issuer directly, from an investment manager, or from an investor relations consulting firm, engaged by the issuer, for providing research coverage for a period of no less than one year. Research articles, as seen here, are part of the service Zacks SCR provides and Zacks SCR receives payments totaling a maximum fee of up to $50,000 annually for these services provided to or regarding the issuer. Full Disclaimer HERE.

________________________

[1] We calculate gross margin as 1-COGS/(revenues from Pylarify, Definity, TechneLite, NeuraCeq and Other Precision Diagnostics) as reported in company filings. We exclude revenues from Strategic Partnerships and Other from the calculation.

[2] The Hatch-Waxman 30-month stay expires in June 2026; however, other barriers may exist.